Thin film solar cells: the way ahead

Despite the current market share remaining low for thin film PV, increased energy demands alongside decarbonisation efforts and energy security concerns, are expected to play a role in driving the uptake of the technology, according to IDTechEx's new report 'Flexible Photovoltaics Market 2025-2035: Technologies, Players, and Trends'.

IDTechEx says a move to newer materials such as perovskite, organic PV, CIGS, dye sensitised solar cells, and amorphous silicon, layered onto a flexible substrate, will not only reduce the reliance on a narrow supply chain (China currently produces around 85 percent of silicon modules, wafers, and ingots), but open up possibilities for integrating solar cells within a number of new applications.

Self-powered electronics, windows, and the sides of buildings, are amongst some examples or where thin film photovoltaics could be integrated to increase power efficiency.

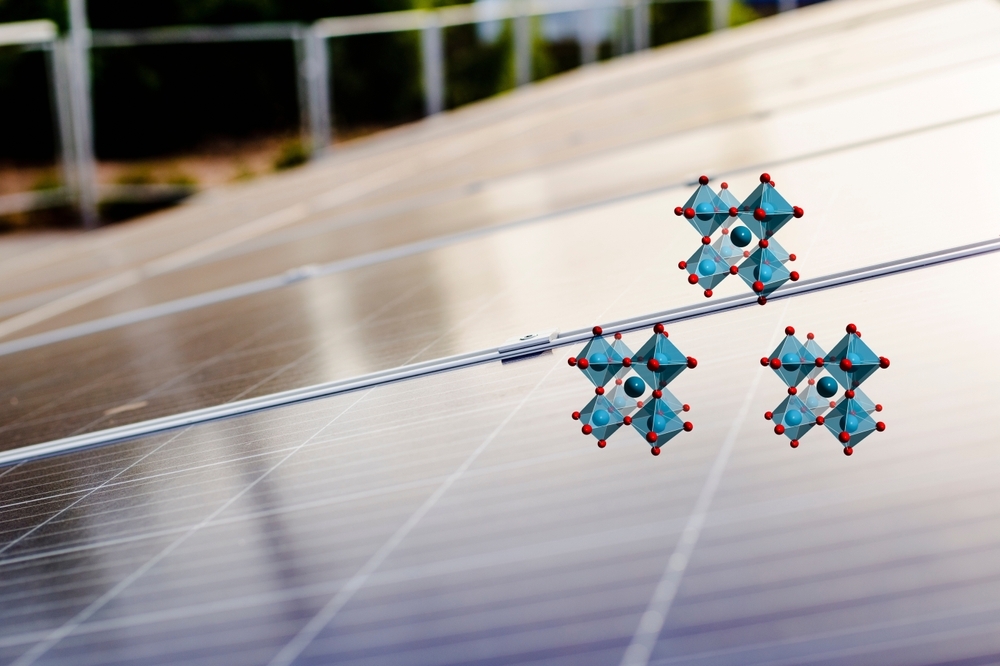

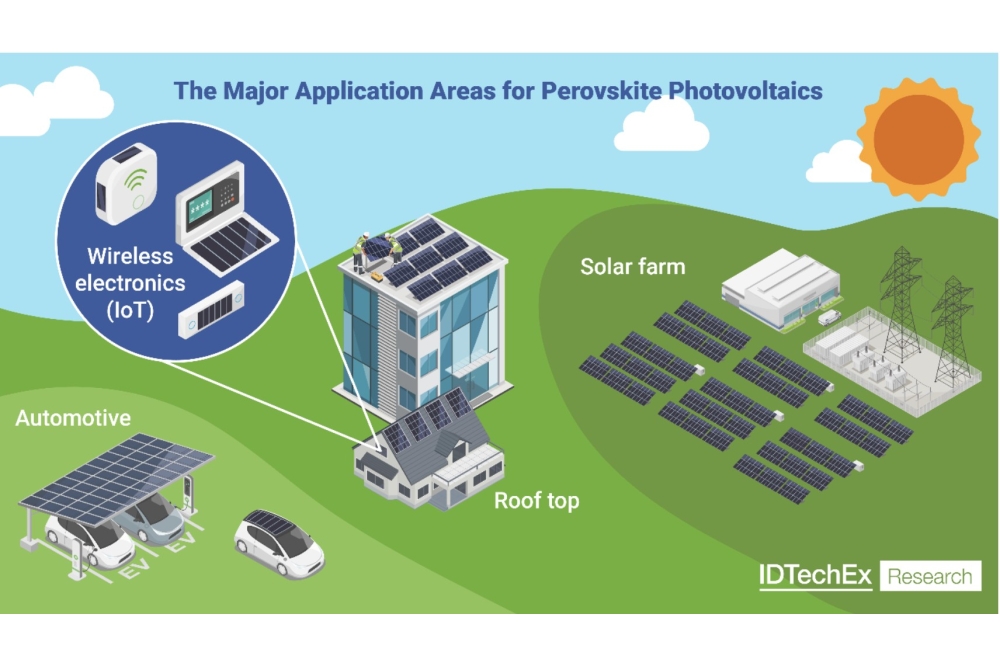

Perovskites are particularly promising as the thin nature of perovskite active layers enables them to be sheet-to-sheet or roll-to-roll compatible, and for applications with weight limitations and the need for flexibility, it could be a preferred material choice. However, IDTechEx states that the benefits and efficiency of perovskite materials for photovoltaics could be best extracted when used as an enhancer for silicon solar panels, to avoid an efficiency plateau.

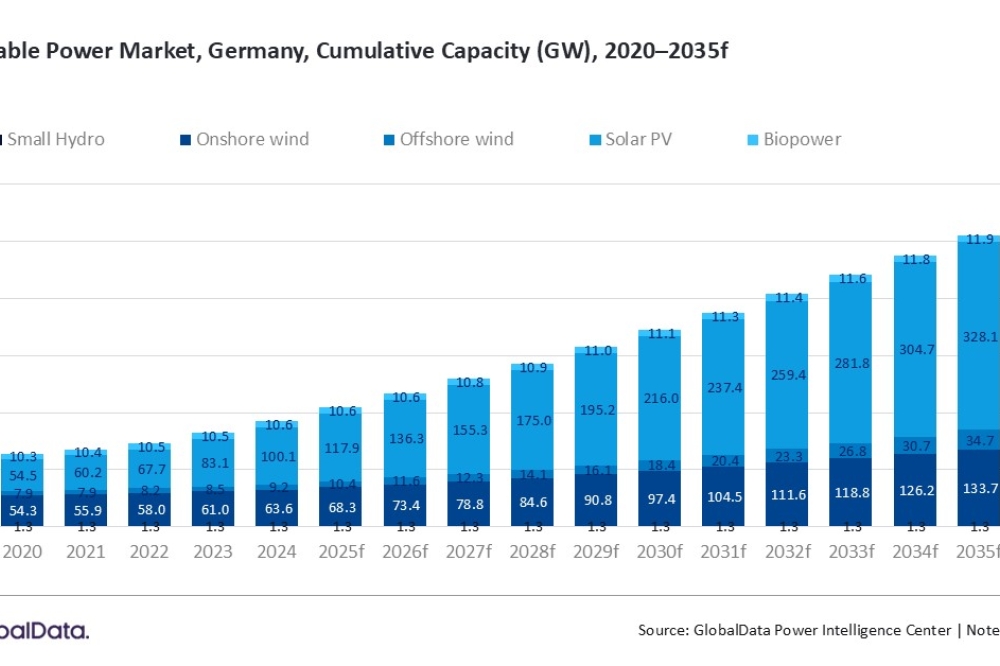

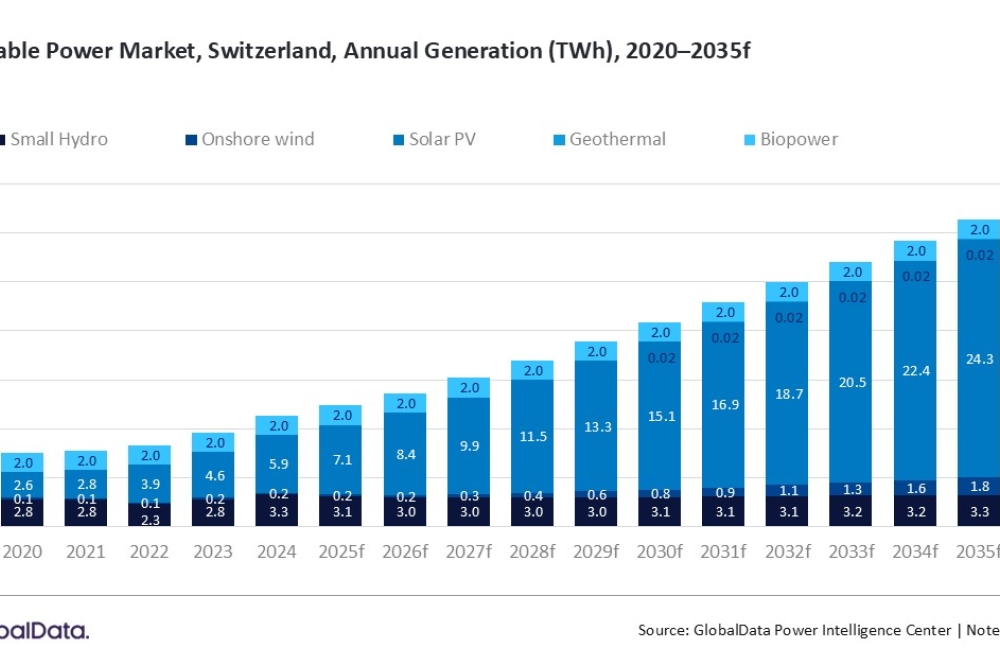

IDTechEx reports in 'Perovskite Photovoltaic Market 2025-2035: Technologies, Players & Trends', that between 2010 and 2023, the solar photovoltaics capacity grew at a compound annual growth rate of 31.8 percent, which was over double that of wind power. One of the largest jumps in growth was between 2022 and 2023, highlighting the more recent investments and government initiatives that have taken place, in line with the trends of sustainability and decarbonisation.